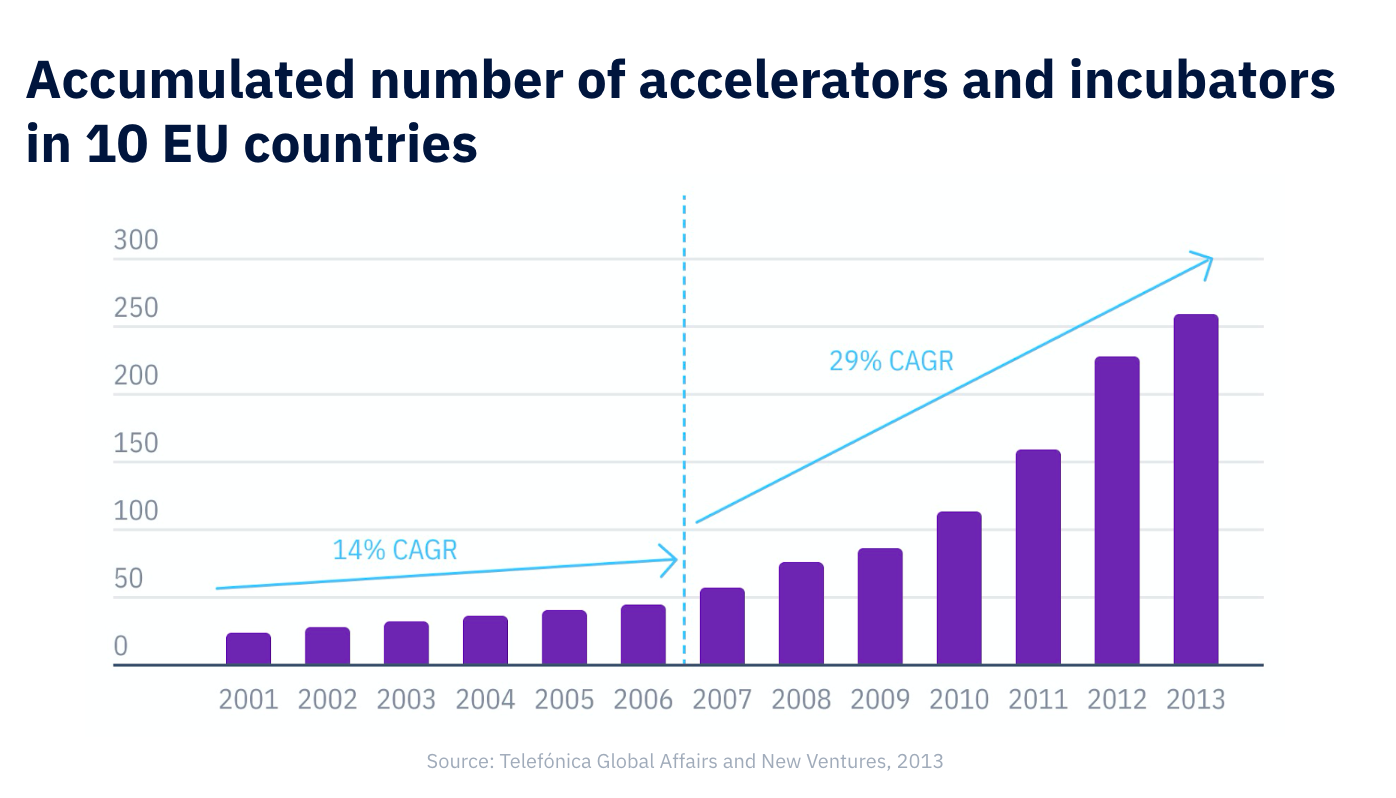

Ever since Y Combinator launched in 2005 in Cambridge, the contagious enthusiasm of accelerating startups has spread across the world. In 2016, Gust reported more than 10,000 accelerators worldwide, and a Telefonica study put the growth of the industry at 30% CAGR.

We’ve seen quite a few situations of new accelerators popping up, copying the YCombinator or TechStars model and expecting that hope (or “spray and pray”, how it’s often called in the investment world) will lead to success. In most cases, within three years, most of these ventures turned into a proper seed fund, an educational program, a corporate marketing initiative, or they just died (unfortunately, there is no clear data of this—maybe we’ll look at it in a further study).

We’ve seen quite a few situations of new accelerators popping up, copying the YCombinator or TechStars model and expecting that hope (or “spray and pray”, how it’s often called in the investment world) will lead to success. In most cases, within three years, most of these ventures turned into a proper seed fund, an educational program, a corporate marketing initiative, or they just died (unfortunately, there is no clear data of this—maybe we’ll look at it in a further study).

“Accelerators are charities, not businesses”

—Jon Bradford, F6S Cofounder, former TechStars London managing director

Jon further argues that it’s hard to employ experienced managers in accelerators (most of the good ones would be better off being a startup founder, or in a corporate job). On top of this, the risk is huge, the equity percentages low, and the return-on-investment is low. Essentially, most accelerators fail to capture the value they are creating.

One of the main reasons is the lack of a set of best-practices for any situation. We’ve tried to compile some of them, but the hard reality is that there are few things that work universally. We’ve found out more bad-practices, such as copying existing models (YC, TechStars, or other successful accelerators), without considering the foundation of any accelerator:

- Talent & know-how (local strong education).

- Industry and business (purchasing power, strategic partnerships)

- Capital (public and private sources)

- Strong networks (personal or professional)

- Culture (risk-aversion, collaboration, innovation, trust etc.)

What private accelerators often forget is that they are startups themselves—startups helping other startups. They have limited resources, tons of assumptions, a business model and approach yet to be validated, and very slim chances to turn into a sustainable, high-growth business.

As a standalone, independent business, a private accelerator has very few chances to stay alive beyond 2-3 years. Even the largest accelerators have low success rates:

- Y Combinator invested in 2,559 startups, of which 260 exited (10%).

- 500 Startups invested in 2,131startups, of which 206 exited (9.6%).

- TechStars invested in 1,797 startups, of which 168 exited (9.3%).

- Plug and Play invested in 938 startups, of which 65 exited (6.9%)

- Startupbootcamp invested in 525 startups, of which 26 exited (4.9%).

These are some of the strategies employed by private accelerators:

- Function as a scouting & de-risking program for pre-seed or seed-stage investments of a seed fund or micro VC.

- Fund operations from other sources (corporate partnerships, educational programs, governmental grants or public funds).

- Create a very strong network for follow-on investments.

- Function as a fund (as strategy, success metrics), but with a high-touch approach for new investments; usually this means no cohorts.

- Charge for participation, instead of taking equity.

Failure can be avoided and, while few accelerators can become successful, building sustainability is possible by choosing the right business model (or transition to the right business model) from the start of the process. It’s a long journey and, most likely, this will be a topic for further research.

Accelerator management tool

- Streamline your deal flow

- Keep all information and communication in one place

- Connect your mentors and founders, and more...